Silver Market Alert

Physical Scarcity and the COMEX/LBMA Dynamics

The silver market is currently exhibiting extreme stress, signalling a significant disconnect between the paper trading on the COMEX exchange in New York and the physical metal market centred in London (LBMA). This stress is being driven by a combination of unprecedented lease rates and arbitrage activity using the Exchange for Physical (EFP) mechanism.

The Problem: Skyrocketing Lease Rates and Price Dislocation

The primary indicator of physical scarcity is the silver lease rate—the cost to borrow physical metal in London. Recent reports show these rates spiking to annualised levels as high as 35% to 39%.

What this means: Holders of physical silver are demanding an enormous premium to temporarily part with their metal, indicating an extreme lack of immediately available supply in the London vaults.

The Dislocation: This scarcity has led to the LBMA spot price trading at a significant premium (reported to be $2.00 to over $2.50) above the COMEX futures price. This differential creates a powerful incentive for market participants to move metal.

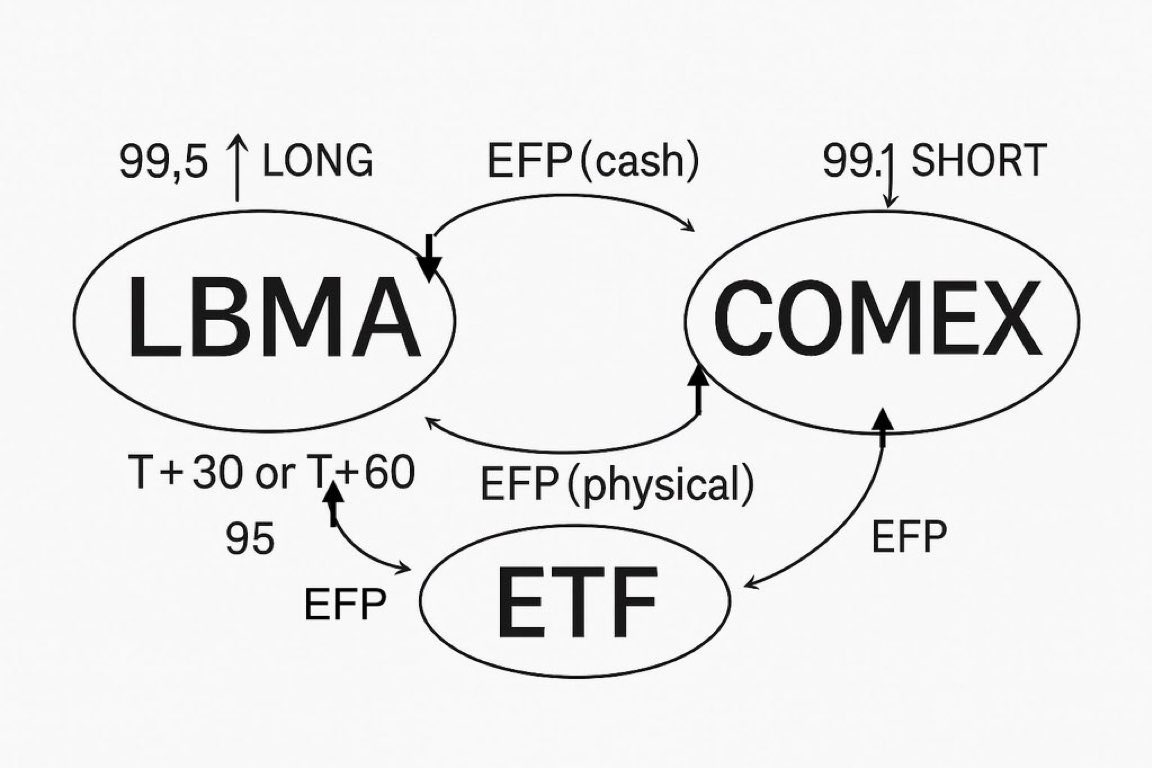

The Mechanism: The EFP and the Arbitrage Flow

The Exchange for Physical (EFP) is a key, privately negotiated transaction that allows institutions to swap a futures position for a physical metal position. When the price difference between London and New York becomes this large, it triggers a major arbitrage opportunity for large institutions, often referred to as Bullion Banks.

Last week’s activity was characterised by this arbitrage:

The Trade: Bullion Banks bought (went long) the cheaper silver futures on COMEX while simultaneously sourcing or selling (going short) the expensive physical silver in London.

The Movement: They then used the EFP to convert their COMEX paper contract into physical metal, which was then shipped from COMEX vaults in New York to London to cover the expensive short position.

The Impact: This action transferred physical silver from COMEX to the LBMA, aiming to profit from the price differential and relieve the acute physical tightness in London.

High lease rates simultaneously forced some short sellers (liquidity providers) to liquidate or “cover” their paper positions on the COMEX, as the cost of continually rolling their positions was becoming prohibitive. This action prevented the COMEX price from dropping significantly despite the selling pressure.

Outlook: Two Scenarios for COMEX Buying Pressure

The underlying dynamics suggest that buying pressure on COMEX futures is set to increase this week, which could lead to a significant move in the silver price.

Scenario 1: Continuation of Arbitrage Flows

As long as the LBMA spot price holds a large premium over COMEX futures, more players will look to execute the arbitrage trade.

To perform this trade, they must buy silver futures on COMEX to secure the metal that will be shipped to London.

Effect: This sustained buying effort directly increases the upward price pressure on COMEX futures contracts.

Scenario 2: Liquidity Providers Cover Their Shorts

The immense cost of borrowing physical silver (lease rates) creates an untenable situation for large players with short positions that need to be maintained or rolled over.

To exit this high-cost trade, these large liquidity providers must buy back their silver futures positions to cover their shorts.

Effect: A coordinated short-covering event acts as a significant injection of buying volume, which could rapidly push the COMEX price higher as the paper market adjusts to the severe tightness of the physical market.

Both scenarios point to a structural necessity to buy COMEX futures, suggesting the market is in a phase where the paper price must adjust to align with the scarcity and high cost of the physical metal.

Conclusion: The Inevitable Price Alignment

The extreme dislocation between the LBMA and COMEX is unsustainable. The market has entered a phase where the financial pressure of 35-39% lease rates and the profit motive of arbitrage are forcing the “paper” price to concede to the “physical” reality.

Whether driven by Bullion Banks buying cheap COMEX futures to sell into the expensive London market, or by short sellers frantically covering their positions to avoid ruinous borrowing costs, the structural necessity is the same: massive buying volume is being injected into the COMEX.

This intense, fundamental demand suggests that the COMEX silver price is facing an inevitable and potentially swift adjustment to align with the scarcity and high premium of physical silver in London. The paper market is currently being dragged toward the truth of the physical market.